Andy Burnham is widely expected to become leader of the Labour Party and Prime Minister – perhaps even in time to watch the World Cup Final from Downing Street on 19 July. For Labour, it is a moment of both relief and danger. Relief, because Keir Starmer’s leadership had become a lightning rod for public anger and frustration. Danger, because changing the face at the top does not, on its own, change what voters think is happening to the country.

The temptation will be to treat Burnham’s arrival as a political reset. Labour MPs, activists and advisers may hope the party has regained some emotional connection with the electorate: a northern voice, a former mayor, and a straight talking politician. After May’s local election results, many in Labour will hope that things can only get better. But our polling data reveals the scale of the challenge facing the party.

In Yonder polling conducted immediately following Starmer’s resignation announcement, just 20% of adults in Britain said they were likely to vote Labour at the next general election (giving a 7 or higher on a 0 to 10 scale of probability), with Reform UK standing at 24%, and the Conservatives on 21%.

Further, Labour is failing to hold together the coalition that put it into office in 2024. Only 51% of 2024 Labour voters say they are likely to vote Labour next time. By contrast, Reform UK is retaining 80% of its 2024 voters, the Greens 79% and the Conservatives are holding on to 65%. Many of those who voted Labour have already drifted away and show little sign of returning.

For businesses, investors and organisations trying to understand the next phase of British politics, a crucial question is not just who leads Labour, but what pressures that leader will face. A weak governing party, squeezed on all sides of the political spectrum, is likely to be more interventionist, more restless and more focused on highly visible, populist demonstrations of change.

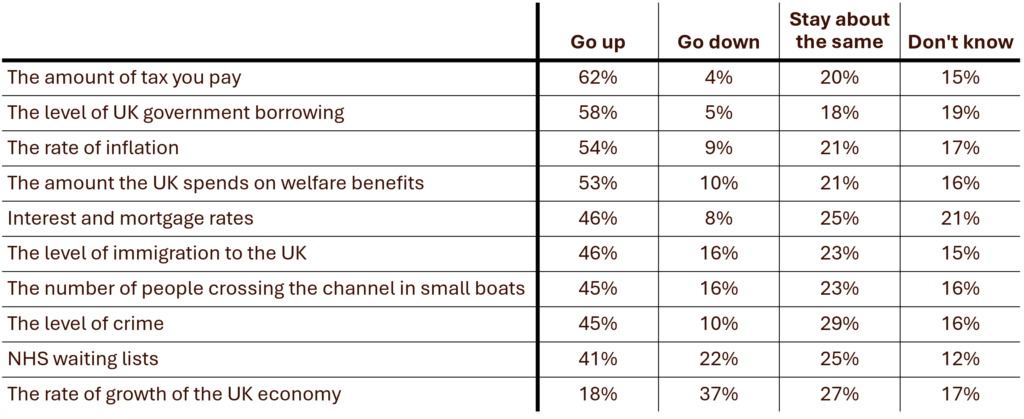

The public mood explains why. Since 2024, Yonder has asked voters whether they expect various measures to go up, go down or stay about the same with Labour in government. The results are bleak. Most voters expect the amount of tax they pay to go up (62%), government borrowing to rise (58%), inflation to increase (54%) and welfare spending to rise (53%). Only 18% think economic growth will go up, while 37% think it will go down.

Figure 1: survey data summary table for the question ‘With Labour in government, will the following things go up, or go down or stay about the same?’

Voters are not merely disappointed with Labour; many still expect core problems to worsen. If households assume taxes, borrowing, inflation, crime, immigration and NHS waiting lists are all heading in the wrong direction, the government starts every argument on the back foot.

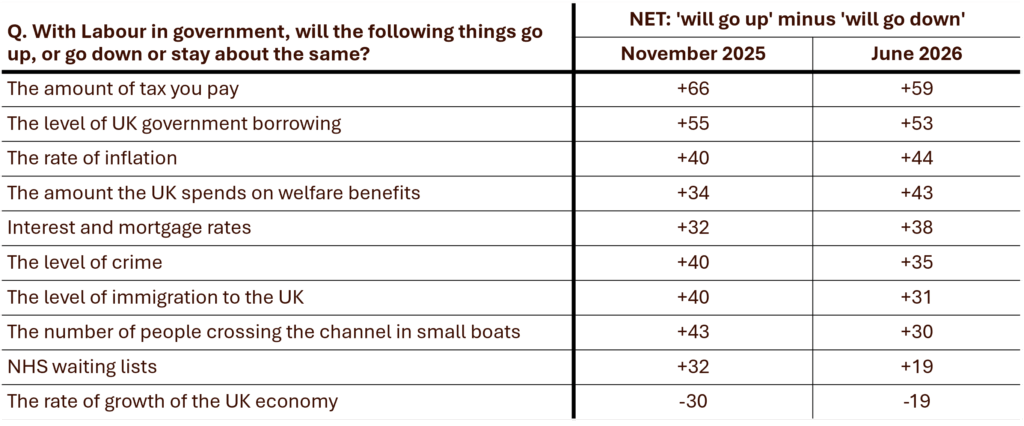

However, there are glimmers of hope for Labour. The picture is less negative than in November 2025. To aid historical comparison, we analyse NET scores (the % who say ‘go up’ minus the % who say ‘go down’). The NET score for people expecting their taxes to go up has fallen from +66 to +59. For small boat crossings, it has fallen from +43 to +30. For NHS waiting lists, from +32 to +19. And on economic growth, the net score has improved (slightly) from -30 to -19.

These numbers suggest public mood may be less hostile compared to late-2025. For a new leader, that matters. Politics is often about direction of travel as much as the absolute position. Andy Burnham may not inherit a positive landscape, but it could be one with room to manoeuvre.

Figure 2: table showing NET: go up scores since 2024 (NET scores are a calculation of the % of respondents saying ‘go up’ minus the % saying ‘go down’)

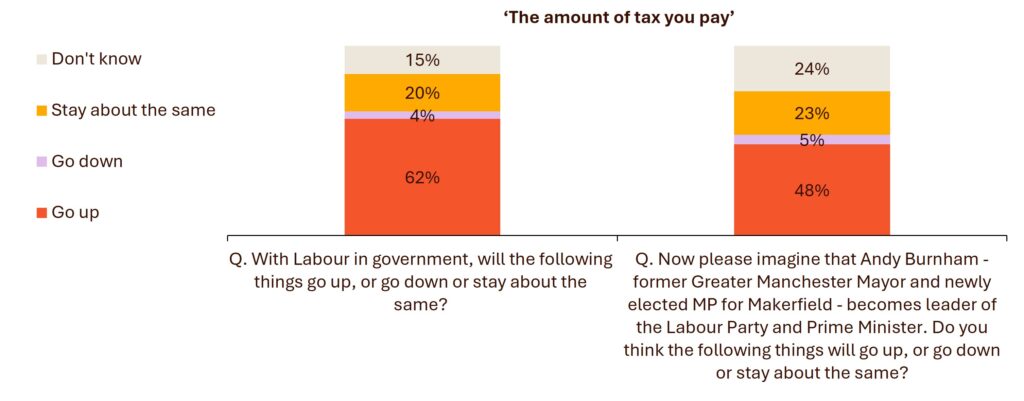

Our polling also suggests that Andy Burnham may soften negative perceptions of Labour, at least in the short term. When voters were asked to imagine Andy Burnham as Prime Minister, perceptions are less negative than when asked simply about Labour in government. For example, 62% expect their taxes to rise under Labour, but that falls to 48% when picturing Andy Burnham as Prime Minister.

Figure 3: comparing perceptions of ‘the amount of tax you pay’ with Labour in government versus with having Andy Burnham as Prime Minister

That uncertainty is valuable, as it gives Andy Burnham an opportunity to define himself before his opponents and events do it for him. However, it is also fragile. Lord Ashcroft’s recent focus groups underline the point: many voters know little about him and are unsure why Labour regards him as its great hope. Some are unsure why a party with a parliamentary majority has turned to someone who, until recently, was not an MP.

The Andy Burnham premiership might begin with opportunity, but not with deep reserves of public confidence. Therefore, his early signals matter. In his speech at the People’s History Museum in Manchester, Andy Burnham set out the idea of a “No. 10 North” focused on reform of essential utilities, reindustrialisation, and regeneration. He also spoke of giving all parts of the UK greater public control over essential services such as water, housing, energy and transport.

For businesses in these sectors, this is cause for concern. A Labour Party under pressure to prove it has changed may look to utilities, infrastructure, housing, transport and energy as arenas in which to demonstrate purpose. Regulation, ownership models, pricing, investment obligations and public accountability could all come under sharper scrutiny.

Andy Burnham’s challenge is simple to state and hard to meet, as he must make Labour feel different before voters conclude that nothing has changed. For organisations trying to navigate the next phase, the lesson is equally clear: do not mistake a leadership change for political stability. The new Prime Minister may enjoy a honeymoon, but it will be brief and the demand for visible, tangible change will be immediate.

Methodology

Yonder interviewed 2,079 adults (aged 18+) in the UK online between 24 and 25 June 2026. Demographic quotas and weights were used to ensure the sample was demographically representative of the UK adult population. Additionally, the survey’s sample of 2024 General Election voters in Great Britain was weighted to represent the known result of the 2024 General Election in Great Britain.

The Green tide: how voter disillusionment is reshaping the UK’s political landscape

The current surge in support for the Green Party is not just a headache for Labour; it’s a symptom of

Labour’s political struggles mean UK businesses should expect net zero contradiction